On June 20, at the 2025 SMM (4th) Electric Drive System Conference and Drive Motor Industry Forum - Main Forum, jointly organized by SMM Information & Technology Co., Ltd., Hunan Hongwang New Materials Technology Co., Ltd., Louxing District People's Government, and National-Level Loudi Economic and Technological Development Zone, Cui Dongshu, Secretary General of the China Automobile Dealers Association Automotive Market Research Branch, delivered a speech titled "World NEV Market Analysis and Future Prospects."

1. Overview of the Global Automotive Industry

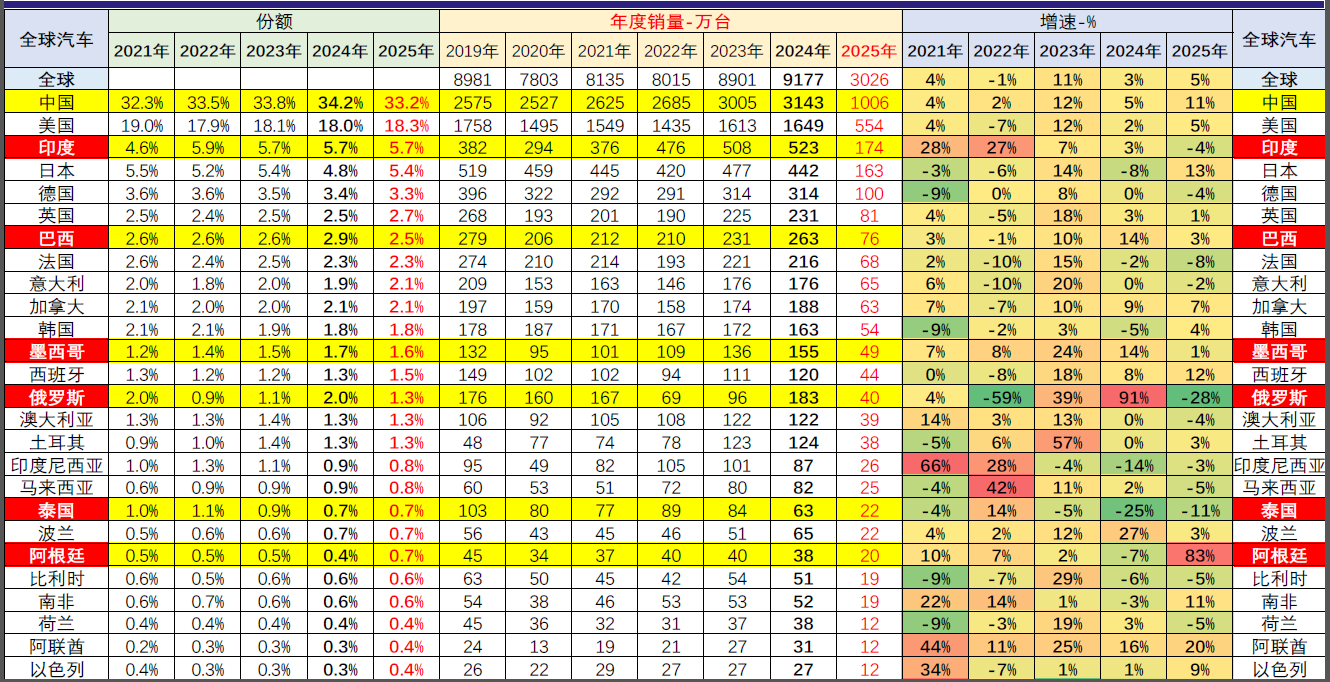

Global auto sales rose 5% YoY, while China's increased 11%, accounting for 33% of the global market, January-April 2025

• The global auto industry peaked in 2017 with sales of 94 million units. During the COVID-19 pandemic from 2020 to 2022, annual sales remained at around 80 million units.

• Post-pandemic global auto sales reached 89.01 million units in 2023 and 91.77 million units in 2024, up 3% YoY.

Diverging trends in global auto markets: contraction in Europe, the US, Japan, and South Korea, recovery in China and India

Dramatic shifts in the global auto market since 2019, with China's rise

• By 2025, leading automakers in Europe and the US saw significant market share declines compared to 2019, while Japanese and South Korean automakers performed slightly better due to the Indian market.

• Chinese automakers like BYD, Geely, Chery, and Changan have steadily increased their global market share.

Comprehensive growth of global NEVs - perspectives from the world and China

• Global NEVs initially developed with hybrid electric vehicles, followed by accelerated growth of plug-in hybrids and pure EVs since 2015.

• In 2025, traditional internal combustion engine vehicles accounted for 73%, hybrids 7%, plug-in hybrids 7%, and pure EVs 13%.

Global trend toward pure electrification - China's share reaches 63%

• Pure EV development represents a common global trend in new energy vehicles.

China's distinctive plug-in hybrid path - nearly 80% global share

• BYD and Geely's strong performance in standard plug-in hybrids, along with Li Auto and Huawei's Seres in extended-range EVs, drove China's nearly 80% global share in plug-in hybrids.

Japanese and South Korean automakers dominate 95% of the hybrid market

• Conventional hybrids, with outdated technology from last century, are led by Japanese and South Korean brands, while Chinese automakers leapfrogged this stage with lithium battery technology.

2. Analysis of China's Auto Market Competition

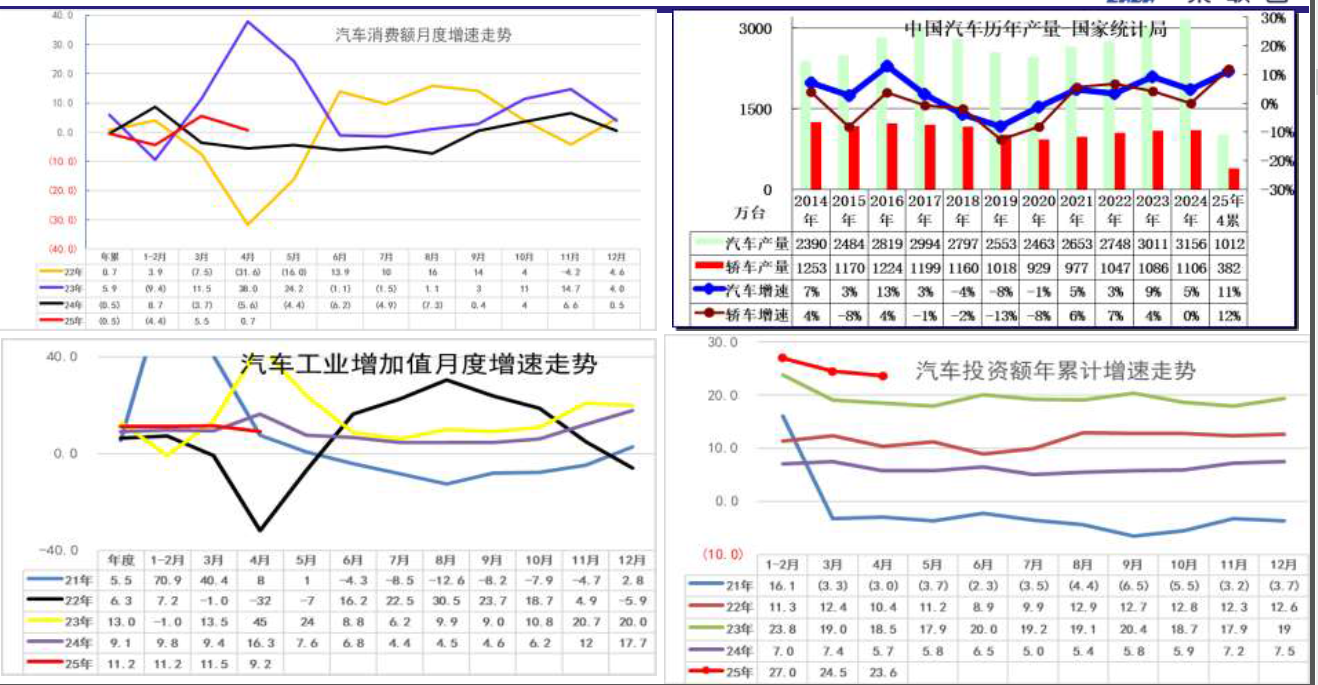

Weak auto consumption in China in recent years

Auto consumption totaled 4.9 trillion yuan in 2023 and 5 trillion yuan in 2024, accounting for 10% of total retail sales and 28% of retail sales by enterprises above designated size.

In April 2025, it represented 9.8% of total retail sales and 26% of retail sales by enterprises above designated size. While China's overall retail sales grew steadily in recent years, auto consumption requires further improvement.

Auto consumption down 1%, production up 11%, value-added up 11%, investment up 24%

China's auto market shifts from state-owned conglomerates to independent automakers

• The automotive industry landscape changed rapidly since 2022 with the rise of NEV manufacturers.

• The previous dominance of SAIC, FAW, and Dongfeng has been completely reshaped by automakers like BYD and Chery.

Major changes in passenger vehicle market structure

• Passenger vehicle sales are projected to reach 28.6 million units in 2025, up 7% YoY, marking five consecutive years of growth since 2021 and hitting a record high.

• Intense competition among automakers, with strong performance by new leading enterprises and significant declines by former market leaders.

Additional details: sedan sales in 2024 were 1 million units lower than in 2014; the MPV market expanded with large models following multi-child policy incentives; SUV sales increased by 10 million units from 2014 to 2024; commercial vehicle sales shrank by 1 million units during the same period.

Trends in China's passenger NEV market

• Domestic NEV retail sales grew from 1 million units in 2020 to 10 million in 2024, achieving a tenfold increase in four years.

• NEV exports also surpassed 1 million units, though currently significantly impacted by EU countervailing duties.

Announcement on extending and optimizing NEV purchase tax reduction and exemption policies

• 1. NEVs purchased between January 1, 2024 and December 31, 2025 are exempt from purchase tax, with a maximum exemption of 30,000 yuan per passenger NEV. NEVs purchased between January 1, 2026 and December 31, 2027 will receive a 50% purchase tax reduction, capped at 15,000 yuan per passenger NEV.

• The purchase date is determined by the issuance date of the uniform vehicle sales invoice or customs duty payment certificate.

• NEVs eligible for purchase tax reduction/exemption include pure EVs, plug-in hybrids (including extended-range EVs), and fuel cell vehicles that meet technical requirements. These requirements are jointly formulated by the Ministry of Industry and Information Technology, Ministry of Finance, and State Taxation Administration based on technological advancements, standard system development, and model changes.

• 2. For "battery swapping" NEVs sold without power batteries, where the NEV and battery are invoiced separately, the purchase tax calculation is based on the tax-exclusive price stated in the uniform vehicle sales invoice for the battery-less NEV.

• "Battery swapping" NEVs must meet relevant technical standards, and manufacturers must provide swapping services directly or through third parties.

The presentation also coveredplummeting battery raw material and battery prices driving vehicle costs down; gradually moderating auto market promotions; exceptionally strong price reductions for new NEV models in China.

Outstanding competitive innovation

Domestic brands demonstrate strong momentum in launching new NEV models.

Plug-in hybrids and extended-range EVs introduced in 2024 performed well in the market.

Strong NEV penetration in China with minimal urban-rural gap

Extended-range and plug-in hybrids dominated in 2024, pure EVs gaining strength in 2025; new automakers rise

The analysis included features of pure EV market trends, plug-in hybrid sales by segment, and overall charging pile status.

Rapid improvement in China's EV charging infrastructure

• Incomplete statistics show public charging piles reached 3.99 million by April 2025, with 10.07 million private charging piles accompanying vehicles.

• Based on the assumption that one public pile serves three EVs, the 2025 combination of public and private piles achieves a 1:1 charging capability for pure EVs.

3. NEV Industry Chain Analysis

Global automotive profit structure - China's disruptive impact

International automakers maintained high profits in recent years, with the automotive sector in the Fortune Global 500 generating $184.9 billion in profits in 2023, a 6.3% profit margin.

The battery industry achieved substantial profits, with CATL and BYD earning $10.4 billion in 2023. Other leading Chinese automakers reported $6.6 billion in profits.

Integration and lightweighting emerge as key motor development directions, with multiple companies adopting multi-in-one solutions

• Increasing demands for driving range, power density, and energy efficiency drive rapid development of integrated, compact, and lightweight electric drive systems.

• With advancing power electronics technology, electric drive systems evolved from initial "three-in-one" to "six-in-one," "eight-in-one," and even "twelve-in-one" configurations, incorporating more integrated components. Multi-in-one systems combine motors, reducers, controllers, and other parts with shared housings and wiring to achieve integration, cost reduction, and weight savings.

China's lithium ore reserves jump to world's second largest

• On January 6, 2025, China's Ministry of Natural Resources announced during a press conference on key achievements of the new round of mineral exploration breakthrough strategy the discovery of the world's first ultra-deepwater, ultra-shallow large gas field, adding over 100 billion m³ of proven natural gas reserves. The campaign also identified 10 new 100-million-mt oil fields and 19

100-billion-cubic-meter-scale gas fields. The exploration and development of deep coalbed methane have entered the fast lane, with proven geological reserves exceeding 500 billion m³.

• China has achieved a series of major breakthroughs in lithium ore prospecting, with the proportion of lithium ore resources in the global total surging from 6% to 16.5%, successfully jumping from sixth to second place in the world. This transformative progress has undoubtedly reshaped the global distribution pattern of lithium resources.

• According to data from the United States Geological Survey (USGS), as of the end of 2023, China's lithium resources amounted to approximately 6.8 million mt in metal content. Although it still ranks sixth globally, this breakthrough in prospecting has undoubtedly won China a more important position in the global lithium resource market. Previously, lithium resources were mainly concentrated in three South American countries (Bolivia, Argentina, and Chile) and the US, which together accounted for two-thirds of the global lithium resources.

• The newly discovered 2,800-kilometer-long world-class spodumene-type lithium metallogenic belt in the West Kunlun-Songpan-Garzê region has enriched the types and distribution range of China's lithium ore resources, forming a new direction for development and utilization, and lithium ore reserves are expected to further increase.

• In addition to spodumene-type lithium mines, significant progress has also been made in the development of salt lake lithium resources. The development of salt lake lithium resources is characterized by low costs and minimal pollution. The amount of lithium resources in salt lakes on the Qinghai-Tibet Plateau has significantly increased, making China the third-largest salt lake-type lithium resource base after the Lithium Triangle in South America and the western US.

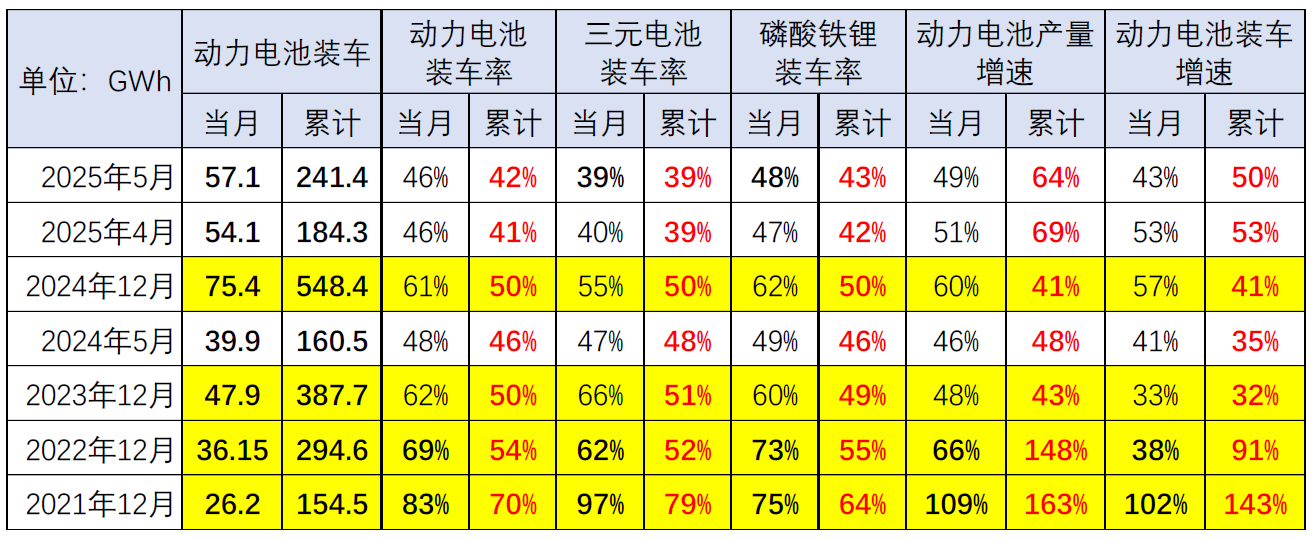

The lithium battery market is expected to be highly prosperous in 2025

An analysis was conducted considering factors such as overall battery production, battery exports, ternary battery production, and LFP battery production.

Analysis of the development status of power batteries

It also introduced content such as changes in battery energy density, changes in the production structure of power batteries, and relatively good gross margins in the battery industry chain.

4. Outlook on Future Policies and Consumer Markets

Uncertainties in the external economic and trade environment are expected to increase in 2025

The world's proven oil reserves continue to grow, and the theory of oil depletion has not been proven.

♦American geologist M. King Hubbert proposed the theory of oil depletion, arguing that the widespread use of automobiles has led to a sharp increase in global oil consumption, with depletion expected within 50 years.

♦Soviet scientists proposed the abiotic oil formation theory, also known as the petroleum origin theory, which suggests that oil is generated through pyrolysis reactions of organic matter in rocks under high temperature and pressure conditions.

♦In 2023, global oil reserves increased by 1.3% to 240.69 billion tons. As of the end of 2021, China's oil reserves were 3.7 billion tons.

Challenges and Opportunities: The Surge in China's Automobile Exports

In 2020, annual sales reached 1.085 million units, representing a year-on-year decrease of 13.1%. In 2021, export market sales reached 2.187 million units, up 102% YoY.

In 2022, export market sales totaled 3.4 million units, up 55% YoY, primarily due to insufficient overseas supply and the significant enhancement of Chinese automakers' export competitiveness.

In 2023, China's automobile exports achieved 5.22 million units, maintaining strong growth with a 54% export growth rate.

In 2024, China's automobile exports reached 6.41 million units, with a 23% export growth rate.

From January-February 2025, China's automobile exports amounted to 970,000 units, up 17% YoY compared to the same period in 2024. In February 2025 alone, exports stood at 420,000 units, up 7% YoY.

The "friends circle" of China's automobile exports has gradually stabilized.

It introduced the ranking of China's automobile export markets over the years based on the most-traded contracts.

It also elaborated on the divergence in private vehicle popularity and the direction for automotive consumption outlined by the Central Economic Work Conference.

The automotive industry's policy support is historically unprecedented.

♦ The scrap policy expansion is expected to cover 5 million units, worth approximately 90 billion yuan.

♦ The replacement policy maintains stable support, targeting 10 million units with 130 billion yuan.

Additionally, it introduced the CPCA's monthly forecast index and satisfaction index, as well as the annual result tracking of CPCA's monthly predictions.

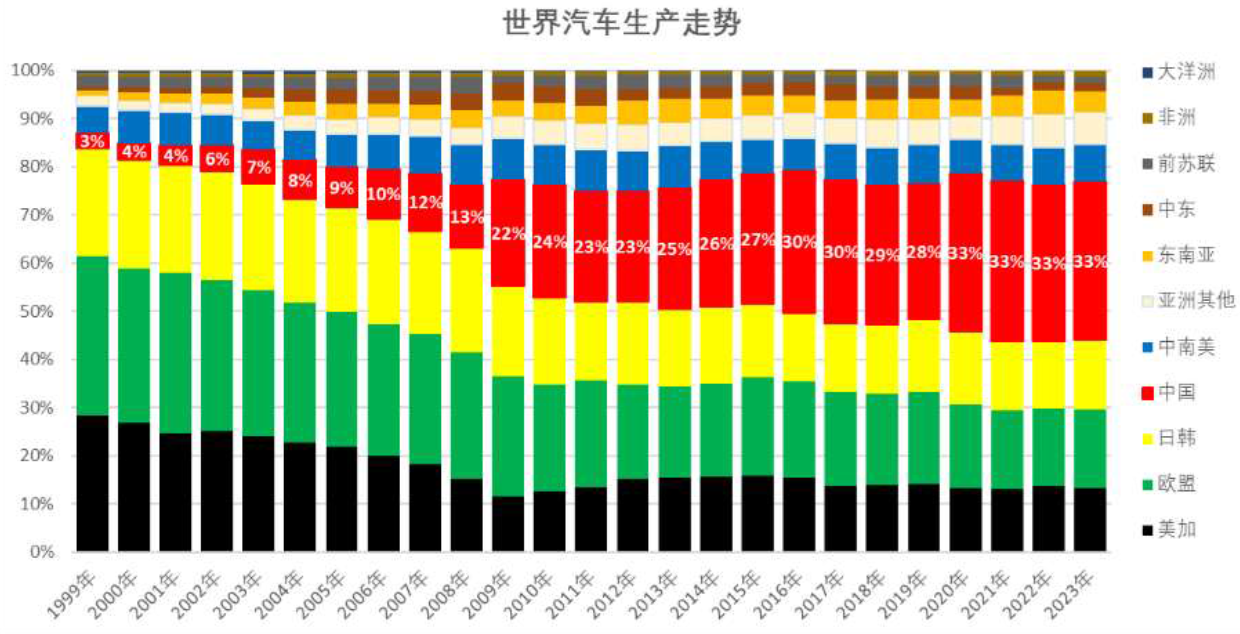

The global automotive production system is shifting from the US, Japan, and South Korea to China and emerging markets.

Future automobiles will undergo significant functional changes.

Automobile positioning: transitioning from mechanical tools to durable electronic consumer goods.

Automobile lifespan: usage cycles will shorten substantially, accelerating replacements.

1. EVs are high-efficiency, low-cost transportation tools;

2. EVs represent an independent third-space ecosystem;

3. EVs serve as ESS units in distributed energy systems.

》Click to view the 2025 SMM (4th) E-Drive System Conference & Drive Motor Industry Forum Special Report